Virtual PPAs and Sleeved PPA Transactions: a Primer

November 10, 2023 – In recent months, Centennial's corporate and industrial customers have increasingly asked for Sleeved PPAs and, in some cases, Virtual PPAs. Instead of re-inventing the wheel, we figured we'd dust off an article written by our Founder's former law firm. With permission of the firm, we're republishing the article below.

But first, here is a quick summary:

-

Sleeved PPAs often involve a direct Power Purchase Agreement (PPA) between the corporate offtaker and the solar project company. The offtaker usually enters into associated arrangements, which are either managed by the offtaker itself or via a utility or other load-serving entity, to enable the output purchased to be used for the benefit of the offtaker's off-site facility load.

-

Virtual PPAs are a financial derivative under which the parties agree a strike price, with payment flows being determined by comparing that strike price against a market reference price. They do not involve the physical delivery of output to the buyer or a utility agent of the buyer.

NORTON ROSE FULBRIGHT

May 2017

Introduction

The article was first published in PFI (April 2017)

Corporate power purchase agreements (PPA) are not a new phenomenon, with the first deals occurring almost ten years ago. However, the size and frequency of deals - particularly in the United States and United Kingdom – has picked up in recent years. Leading global corporations are now looking at new markets for energy procurement solutions.

The suitability of a corporate PPA solution in a particular market is dependent on a variety of factors. In some, it can offer an attractive diversification to developers or their existing options for the offtake of power. In others, it can offer a solution for which the current market cannot provide. However, in many jurisdictions there are commercial or regulatory hurdles that make it difficult for corporate PPAs to be deployed.

The term corporate PPA can capture a range of renewable energy buying structures but we see continued acceleration globally in off-site power purchase agreements between corporate buyers and renewable energy projects. We take a look at the drivers for them, the main types of contract structures used and likely future developments.

Buy-side drivers

From the buy-side, key drivers are environmental and economic.

Environmental

A corporate PPA can assist in the delivery of a corporation’s sustainability commitments. Large numbers of corporations have set ambitious targets for renewable energy sourcing or emissions reduction – whether via leading organisations such as RE100 or independently. Meeting these commitments can be done relatively simply through the purchase of green power products from their utility supplier or procuring renewable energy certificates matching their needs (such as Renewable Energy Certificates in the United States or Guarantees of Origin in the European Union). Some corporations want to go beyond purchasing schemes, looking for opportunities by which they can demonstrate additionality.

Approaches to additionality can differ but in most cases it turns on the idea that the entry into the PPA by the corporation is a material reason for a renewable energy project occurring (such as offering a long term price to a greenfield renewable project) or further projects occurring (such as enabling a refinancing to free up capital for further investments). A recent example of an “additional” PPA is Nestlé UK’s entry into a long term PPA with Community Wind Power for a greenfield Scottish onshore wind project, under which up to 50% of Nestle UK’s electricity requirements can be met.

Economic

A long term corporate PPA with the right pricing structure can also provide a hedge against rising electricity costs. A number of early corporate PPAs adopted relatively straight forward pricing structures, such as a fixed price which can escalate in line with inflation. Although acting as an important hedge if prices rise, these also bear risk if markets move lower. In some markets this has driven more sophisticated pricing structures that allow for price re-openers if there are significant market movements. Other approaches include floating price structures with a cap and floor to provide mutually acceptable risk mitigation for the parties.

Sell side drivers

From the sell-side, the need or interest in a corporate PPA is often driven by wider market design aspects for renewable projects.

Long term revenue certainty (for finance)

Markets which have seen the greatest growth, such as the United States and United Kingdom, are ones where subsidy support for renewables leaves projects with the need to optimise their electricity sales. In the US, this is because support has been provided through tax credits. In the UK, this was the case under the previous green certificate regime known as the Renewables Obligation. Finding a long term solution for power offtake that includes sufficient revenue certainty is key to accessing limited recourse finance. In these markets, long term PPAs with utility offtakers are available. However, corporate PPAs can diversify these offerings. In the right circumstances they can, for example, provide a better floor price (or fixed price) for a project than is available in the market generally (although that may come at the cost of future upside value).

Longer term prices

In other markets, a corporate PPA can solve a particular market issue. A good example of such an issue is the Netherlands, where the floor value on the government support regime creates a risk for projects in the scenario of a future low price market. This is not something utility offtakers have usually been able to solve. Corporate offtakers have been able to do so, as evidenced by the recent multi-buyer transaction with the Krammer wind park. The corporate buyers can take this risk on as they are naturally hedged in that a low price environment is also one which will have wider benefits for the corporations involved (as their electricity costs in the Netherlands will generally be reduced).

The mutual interest in long term price certainty will be very relevant as some markets move to remove subsidies for certain mature renewable energy technologies. Even where cost reductions for a technology type have arguably enabled prices for renewable energy assets to reach parity with grid prices, the need for long term revenue certainty for power sales remains key to bankability. Bankability captures the idea that a project has a sufficiently balanced risk profile that lenders are willing to finance it. Revenue contracts such as a PPA are key to this assessment. A corporate PPA can offer bankability, thus providing an important bridge to the development of wider and more diverse financing and offtake solutions in the market, particularly those that bear a greater degree of merchant risk.

New market opportunities

Beyond these immediate economic drivers, there are a wider reasons for developers being interested in entering into long term transactions with corporate buyers. Some corporate buyers are attracted by corporate PPAs in emerging markets where they have facilities. Developers operating globally or regionally may have plans to accelerate development in these markets. This creates opportunities for wider partnerships between developers and corporate buyers whereby a corporate buyer’s strategic ambitions for corporate PPAs are delivered by the developer. The structure of these partnerships can take a variety of approaches. Some involve delivery by the developer of the target capacity across selected jurisdictions (often encompassing both onsite and offsite solutions). Others operate more as a management service by which the developer locates quality opportunities.

Contract structures

Corporate PPAs can be broadly broken down into two types: synthetic / virtual PPAs and sleeved or physical PPAs.

Synthetic or virtual PPAs

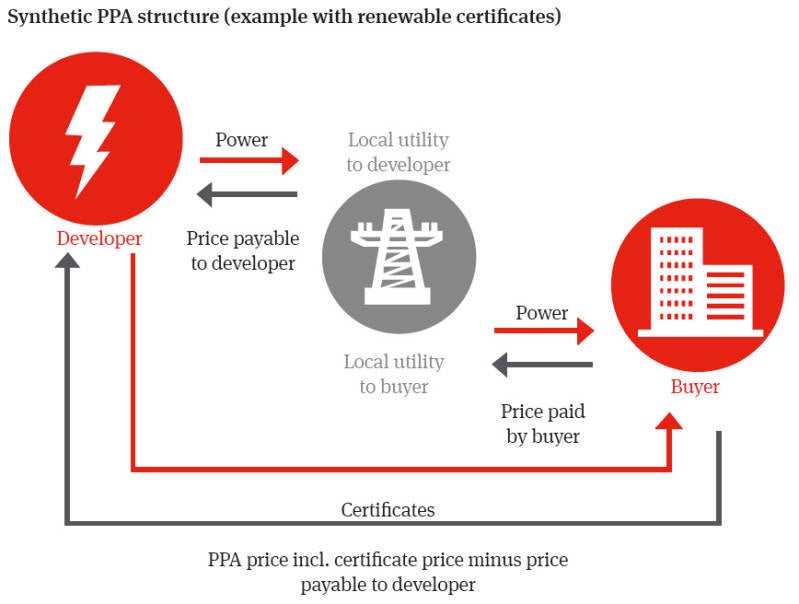

Source: ‘Corporate Renewable Power Purchase Agreements: Scaling up Globally’ A report produced by World Business Council for Sustainable Development (WBCSD), in conjunction with Norton Rose Fulbright and EY

The first type is referred to as “synthetic” or “virtual” PPAs. These are a financial derivative under which the parties agree a strike price, with payment flows being determined by comparing that strike price against a market reference price. They do not involve the physical delivery of output to the buyer or a utility agent of the buyer. There is a wide range of possibilities regarding how these can be structured. For example, they may be two way or one way. In the former, where the market reference price is higher than the strike price, the generator pays the difference to the buyer. Where the market reference price is lower, the buyer pays the difference to the generator. The volume contracted under the agreement can also be specified in a variety of ways and need not be tied completely to the actual generation of the project. This is known as a contract for difference.

There is usually one physical aspect in a synthetic PPA. The corporate buyer will usually need the green certificates awarded to the project for the purposes of demonstrating the renewable nature of the electricity to be delivered to the buyer. These will be used to record against their overall electricity usage and thereby demonstrate the performance of the corporate buyer against their commitments. Some transactions have taken different approaches to this. For example, the corporate buyer may separately purchase green certificates and allow the project to sell the green certificates issued to it.

Source: ‘Corporate Renewable Power Purchase Agreements: Scaling up Globally’ A report produced by World Business Council for Sustainable Development (WBCSD), in conjunction with Norton Rose Fulbright and EY

The second type is referred to as “sleeved” or “physical” PPAs. These often (but not always) involve a direct PPA between the corporate buyer and the generator. The corporate buyer usually enters into associated arrangements (either managed by the corporate buyer itself or via a utility) to enable the output purchased to be used for the benefit of the corporate’s wider facility load.

This is the approach normally adopted in the United Kingdom (although the UK has seen synthetic PPAs). Under this approach, the corporate buyer enters into a PPA with the generator. The corporate buyer simultaneously enters into a PPA with its incumbent energy supplier. This second PPA requires the utility to act as the buyer’s agent in managing the offtake of power from the generation facility. Generally the design of the linked PPAs is intended to mitigate risk for the corporate buyer by passing through obligations and liabilities to the extent possible. Usually the corporate buyer will agree with the utility how the intermittent electricity output of the generation facility will be credited against the corporate’s electricity requirements. This will generally involve management fees associated with the intermittent nature of that generation output. Although this approach has been common to date, it is not the only approach possible. The author is currently developing alternative approaches which offer a far more standardised and stream- lined approach to overcome some common issues in the UK market, including the long negotiation period required to document sleeved transactions and the difficulties in making those work for multi-buyer structures. Multi -buyer structures involve using more than one corporate buyer to support a project, either by having a number of parallel PPAs with different corporate buyers or the establishment of a single buying vehicle that multiple corporate buyers then participate in.

An example of a simpler approach for physical PPAs is provided by the Netherlands. In the Netherlands, a number of corporations are already actively engaged in the wholesale electricity market to manage their electricity requirements. They either directly or via existing service providers. In this context, corporate PPA structures can involve a single PPA between the generator and the corporate buyer. That said, there are usually associated arrangements by which a agent manages the nomination process between the seller and the buyers for the purposes of the wholesale electricity market.

Interaction with policy environments

Corporate PPAs to date have generally developed in markets with existing government support for renewable generation. However, in some markets this is a challenge. For example, where incentives provide a fixed price such as a feed in tariff, generators are less likely to be incentivised to seek corporate buyers offering a fixed price or a price hedge. This is because the need for a long term offtake solution has been removed. Another example is where the government (or a government agent such as a government owned utility) supports renewable generation roll-out by competitively offering long term contracts to eligible projects. In this case there is usually not a place for corporate buyers to be involved in such a structure.

In the recent report from the World Business Council on Sustainable Development (WBCSD) on corporate PPAs that Norton Rose Fulbright co-wrote with EY and the WBCSD, a number of policy recommendations were made. A key one in our view is that renewable incentives should be designed to cost effectively support the development of renewable electricity projects but without removing the drivers for a corporate PPA model. By ensuring there is a place for corporate PPAs, the speed and scale of the deployment of renewable energy projects can be enhanced whilst often diversifying national or regional power markets.

This should be able to occur in conjunction with existing approaches. For example, in countries where PPAs are offered by the government to renewable generators, it is feasible to design PPAs so that the government buyer could offer an opportunity to participate on the buy side to corporate buyers. That could either be by way of back to back arrangements with selected corporate buyers and particular projects or by enabling selected corporate buyers to enter into direct PPAs with a sub-set of the overall pool of projects procured. We understand this is being seriously considered in markets such as Mexico. Designed correctly, such structures could potentially defray part of the expense to government of renewable energy support. That said, corporate demand cannot be assumed to be a substitute for the need for government support for renewables in developing markets. Rather, these two factors need to work in conjunction.

More widely, policy makers should not take steps that can actively frustrate the role for corporate PPAs. For example, the draft text of the updated Renewable Energy Directive for the European Union released in late 2016 includes a provision that would prevent guarantees of origin being issued to renewable energy generators that received any state support. Guarantees of origin are used in the European Union to certify that generated electricity is renewable. Instead, those guarantees of origin would be auctioned and the revenues used to reduce the costs of state support. The effect of this approach would be to frustrate the ability of generators entering into a corporate PPA to deliver guarantees of origin to the buyer. Without these, the buyer would not be able to demonstrate to third parties in an objective manner that the power purchased was renewable. There is a long period before these changes are introduced and it is therefore likely that the final approach will be modified. There are approaches that could be taken to achieve the European Commission’s objectives (which relate to state aid concerns) without disenfranchising renewable generators from the right to be issued guarantees of origin.

Future developments

The commitment of significant global corporations to using corporate PPAs as part of a bundle of approaches to renewable energy procurement is not likely to diminish in coming years. Although some have queried the depth of this market, there remain significant opportunities for these leaders to drive developments in new markets. This is supported by the increasing evidence of global corporations starting to work with their key suppliers to increase the uptake of renewable energy along the supply chain.

We also expect to see innovative transactions in markets such as the United Kingdom supporting subsidy free renewable electricity projects and project development. We also expect to see increased focus on multi-buyer structures, particularly those that can assist move away from large global corporate buyers to groupings of local or regional companies. As these structures are developed, there are likely to be targeted interventions by government that could support the accelerated roll out of corporate PPAs.